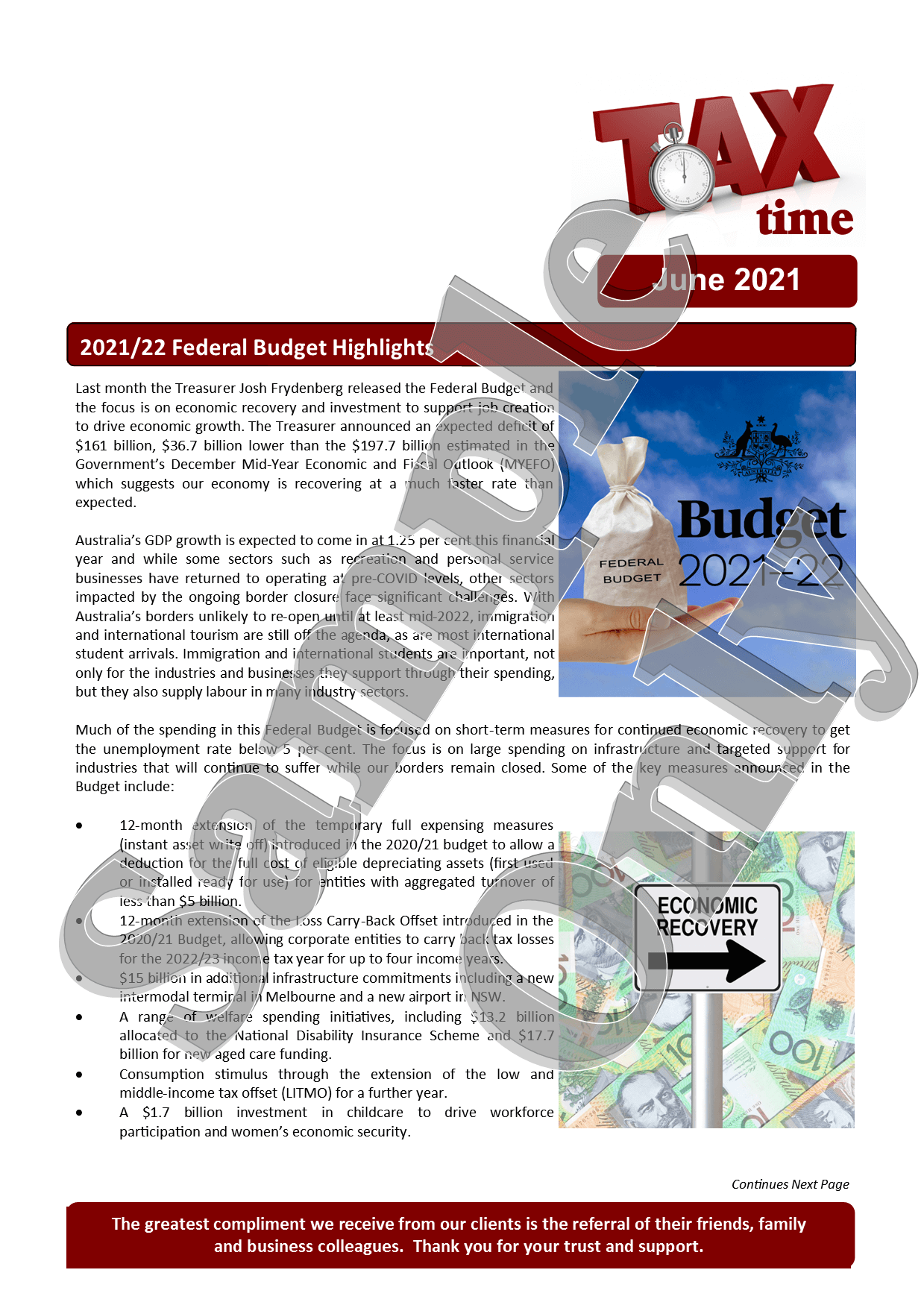

Thinking of Buying an Accounting Practice in 2017?

T he demand for fees is at peak levels in 2017 and if you’re thinking of growing your practice by acquisition here’s some key points to consider:

he demand for fees is at peak levels in 2017 and if you’re thinking of growing your practice by acquisition here’s some key points to consider:

1. Understand why you are buying another firm

The shortage of supply in the last few years has seen buyers jump at anything that lists on the market. My advice is don’t try and push square pegs into round holes and if the profile of the practice or the fee parcel doesn’t fit your strategic plan, you need to step back and revisit your objectives. Ask yourself, how will this acquisition strengthen your core business? Most acquisitions that take a firm in a new direction fail to produce the desired financial results. If you cannot articulate how the transaction will make the firm economically better, it might be better to walk away.

If you’re simply buying because your firm is flat lining or in decline then you might be buying a short term ‘band aid’ solution. If you’re buying a baby boomer’s practice you could be buying into another ageing client base and it’s only a matter of time before that client base starts to retire, sell their businesses and natural attrition kicks in. You might need to address your marketing first to rejuvenate your ageing client base and re-ignite your referral engines otherwise you could end up with double trouble in a few years.

2. Does the firm have previous acquisition experience?

Experience tells us that first-time buyers make financial and operational mistakes. It’s like anything, we learn from our mistakes but when you’re investing hundreds of thousands of dollars in someone else’s practice you need to minimize the mistakes. You might need to hire a consultant or broker who could save you a lot of time in sourcing the right practice, hold your hand through the buying process and provide you with the necessary checklists. A good advisor will make sure that the deal continues to flow and help you maintain your calm and sanity during the negotiation process.

3. Think about integration issues upfront.

I have often said that it is not the acquisition itself that’s hard, it’s the integration. This is when deals begin to unravel. My experience with acquisition is that the real work begins with the integration. No matter what you call the transaction, a takeover, buyout or merge, one party or one culture will be dominant. Determine what that culture will be, what processes will be used and what systems will remain before you sign the contract.

4. Identify upfront the key staff.

Accounting mergers are all about transitioning the people and client relationships. Make sure that you identify the key staff upfront and let them know that they are important to the future of the firm. The number one thing going through everyone’s mind during a merger is ‘What will happen to me?’ You need to answer that question for the key people in the firm and reassure them that their role is safe.

You’ll find the staff are usually the last people to be notified of the sale by the vendor because they don’t want the staff to jump ship. Key staff add value to the sale because they have relationships with clients and having worked on client files, they understand the client jobs.

5. Do you really know the vendor?

Don’t tell me you looked in the seller’s eyes and decided that this was going to be a match made in heaven. My experience is that a sale transaction generally takes at least a month depending on the size of the transaction. That gives you sufficient time to assess the chemistry, their business and ethical beliefs. Most importantly, you’ll learn a lot about the vendor from the behaviour during the negotiation process.

6. Don’t let emotions rule.

Smart buyers identify all the deal-breakers up front. They know when to walk away from a transaction because they have done their due diligence on the market, the prospects and the price they are willing to pay. Don’t chase a practice simply because it is the only one available at that moment in time or you have been the under bidder on the last three opportunities. Patience pays off.

7.Develop a ‘letter of offer’ that is critical for future negotiations.

Your letter of offer should outline the key financial and non-financial terms of the sale and should be non-binding. In other words, you and the vendor have the right to terminate the transaction at any time without any penalties. Any such offer should be subject to a satisfactory due diligence process and finance approval.

If you’re thinking of buying a practice or a parcel of fees you can register your interest with us by completing the buyer's registration form and confidentiality agreement on our website under the services - practices for sale tab.

-P-J-Camm-banner.jpg)

THE MARKETING MUST HAVES FOR ACCOUNTANTS

Marketing Secrets of Successful

Accounting Firms Revealed

Leave a Comment